Microfinance for Sustainable Cities

Financial Inclusion for Urban Sustainability

| Hari Srinivas | |

| Policy Analysis Series E-266 |

|

Abstract: This document examines how microfinance and financial inclusion can support sustainable urban development by linking financial services with environmentally responsible livelihoods, resource efficiency, and community resilience. Using the FEWW nexus of food, energy, water, and waste as a guiding framework, it highlights practical approaches for supporting green microenterprises, household sustainability investments, decentralized community services, and climate adaptation initiatives. The document also explores the roles of institutions, innovative financing mechanisms, monitoring systems, and policy frameworks in advancing inclusive, resilient, and resource-efficient urban communities aligned with the Sustainable Development Goals (SDGs).

|

|

Keywords: Microfinance; Financial Inclusion; Sustainable Urban Development; FEWW Nexus; Urban Resilience; Circular Economy; Climate Adaptation; Community-Based Development |

1. Why Microfinance Matters for Urban Sustainability

- Supports low-income households in managing environmental risks

- Enables access to basic services and technologies

- Promotes inclusive and local economic development

Furthermore, environmental risks and climate change impacts disproportionately affect low-income groups. These populations often live in informal settlements located on marginal, hazard-prone lands, such as steep slopes or low-lying floodplains, with little to no municipal protection.

To address these vulnerabilities, microfinance requires a broader operational approach. Microfinance can enable proactive climate adaptation and resilience-building, moving beyond its traditional focus on basic income generation or survival needs. When properly structured, microfinance can empower communities to build sturdier shelters, secure clean resources, and withstand environmental shocks.

This broader understanding of microfinance aligns closely with several United Nations Sustainable Development Goals (SDGs), particularly those related to poverty reduction, clean energy, sustainable cities, and responsible resource use, as laid out in Table 1.

| SDG | Goal | Role of Microfinance |

|---|---|---|

SDG 1 |

No Poverty |

Microfinance helps low-income households strengthen economic resilience by providing access to credit, savings, and insurance mechanisms that reduce vulnerability to financial and environmental shocks. It also supports livelihood diversification and small enterprise development, helping families move beyond survival-level incomes. |

SDG 7 |

Affordable and Clean Energy |

Microfinance enables households and micro-enterprises to adopt affordable clean energy technologies such as solar home systems, clean cooking stoves, and energy-efficient appliances through small loans and pay-as-you-go financing models. This reduces dependence on expensive and polluting energy sources while improving household health and productivity. |

SDG 11 |

Sustainable Cities and Communities |

Microfinance supports localized urban upgrading by financing incremental housing improvements, community sanitation systems, water access infrastructure, and neighborhood-based enterprises. It also strengthens the resilience of informal settlements by enabling communities to invest in safer and more sustainable living environments. |

SDG 12 |

Responsible Consumption and Production |

Microfinance encourages circular economy practices by supporting recycling enterprises, repair services, composting activities, and sustainable small-scale production systems. It also promotes resource-efficient consumption patterns through investments in water-saving, energy-efficient, and waste-reducing technologies. |

| Case examples | ||

|

Case Study 1: Solar Microfinance Initiatives in India

|

Case Study 2: Waste-Picker Cooperatives in Pune, India

|

Case Study 3: Community Sanitation Financing in Dhaka

|

Microfinance therefore represents far more than a poverty reduction mechanism within the context of sustainable urban development. When linked strategically to environmental resilience, basic service access, and localized economic systems, it becomes a practical tool for enabling inclusive urban transformation.

By supporting household adaptation, strengthening community livelihoods, and encouraging resource-efficient practices, microfinance can help cities advance toward sustainability goals while ensuring that low-income populations are not excluded from the transition to greener and more resilient urban futures, particularly in relation to urban systems such as food, energy, water, and waste.

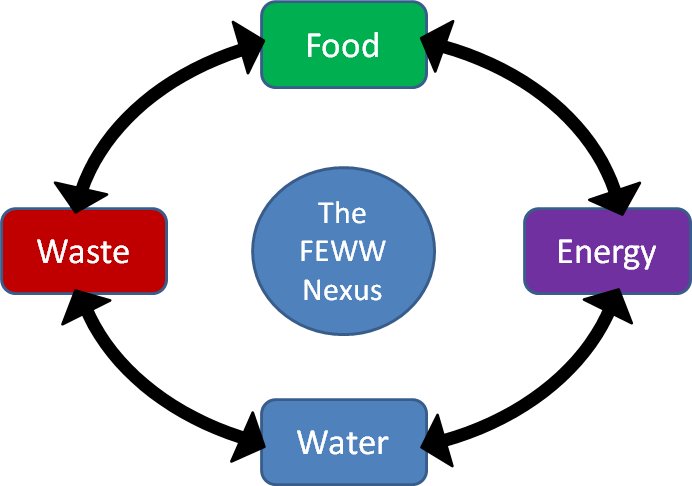

2. Conceptual Shift: From Urban Systems to Household Systems

- Water: Access, storage, reuse

- Energy: Clean cooking, solar solutions

- Waste: Recycling, reuse, informal sector roles

- Food: Localized small-scale urban farming, local food systems

One useful way to operationalize this shift is through the FEWW nexus, which integrates food, energy, water, and waste systems at the local levels.

- Food: Supporting localized, small-scale urban farming, vertical gardening, and micro-capital for small-scale food vendors to secure local food systems.

- Energy: Shifting focus from centralized electrical grids to decentralized, clean household energy solutions, such as clean cooking stoves and solar home systems.

- Water: Moving from large-scale municipal grid expansion to enabling micro-level access to clean drinking water, efficient storage systems, and greywater recycling/reuse at the household level.

- Waste: Transitioning from large municipal landfills to supporting community-level recycling initiatives, upcycling enterprises, and formalizing informal sector livelihoods.

Figure 1: The FEWW Nexus

| Case examples | ||

|

Case Study 4: Household Rainwater Harvesting in Indonesia

|

Case Study 5: Clean Cooking Finance in Kenya

|

Case Study 6: Neighborhood Composting Initiatives in Brazil

|

This household-scale approach transforms sustainable urban development from a large-scale infrastructure challenge into a set of practical, local actions that can be implemented incrementally.

By linking microfinance with the interconnected systems of food, energy, water, and waste, cities can support locally grounded solutions that strengthen livelihoods, improve environmental performance, and build resilience among vulnerable urban populations.

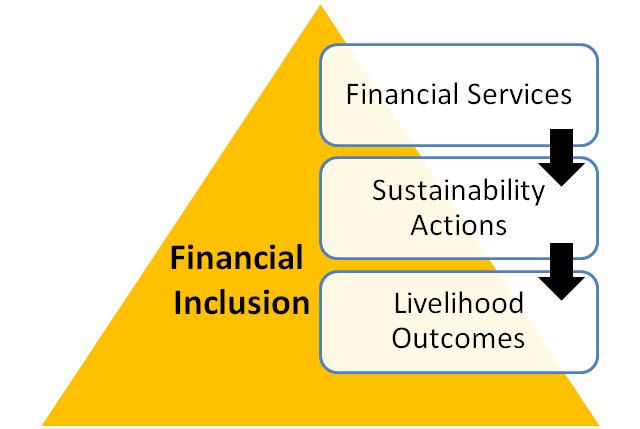

3. The Microfinance-Sustainability Nexus

- Financial Services: credit, savings, insurance

- Sustainability Actions: efficient technologies and practices

- Livelihood Outcomes: income stability and resilience

Core Idea: Financial inclusion can drive sustainability when linked directly to resource-efficient practices and local livelihoods.

- Financial Services: Credit provides targeted micro-loans for green upgrades, while savings accounts help households build adaptive capacities/reserves for future shocks. Insurance mechanisms, particularly micro-insurance, protect assets and livelihoods from climate-related disasters and other unexpected risks.

- Sustainability Actions: Communities adopt efficient technologies such as LED lighting, water filters, and solar devices to reduce costs and environmental impacts. Circular practices, including composting, waste segregation, and material upcycling, further strengthen local sustainability and resource efficiency.

- Livelihood Outcomes: These combined efforts contribute to greater income stability through lower utility costs and diversified revenue streams. They also reduce vulnerability by improving health conditions, creating safer housing environments, and strengthening resilience against social, economic, and climate-related shocks.

These interconnected relationships can be organized into three operational dimensions linking finance, sustainability practices, and livelihood outcomes, as illustrated in Table 2.

Figure 2: Microfinance and Financial Inclusion

| 1. Financial Services | 2. Sustainability Actions | 3. Livelihood Outcomes |

|---|---|---|

|

Credit: Targeted micro-loans for green upgrades. Savings: Secure accounts to build resilience reserves. Insurance: Micro-insurance to protect assets from climate disasters. |

Efficient Tech: Adoption of LED lighting, water filters, and solar devices. Circular Practices: Composting, waste segregation, and material upcycling. |

Income Stability: Lower utility costs and diversified revenue streams. Reduced Vulnerability: Improved health, safer housing, and shock-resistant livelihoods. |

| Case examples | ||

|

Case Study 7: Climate Micro-Insurance in the Philippines

|

Case Study 8: Green Enterprise Financing in Vietnam

|

Case Study 9: Women's Recycling Cooperatives in Colombia

|

The relationship between financial inclusion and urban sustainability becomes most effective when financial services are directly connected to practical environmental actions and livelihood improvements.

By integrating credit, savings, insurance, and resource-efficient practices within local economic systems, microfinance can support not only poverty reduction, but also the development of more resilient, inclusive, and environmentally sustainable urban communities.

4. Key Intervention Areas

- Green Microenterprises: recycling, repair, eco-services

- Household Investments: solar systems, water filters

- Community Services: shared sanitation, waste systems

- Women and Youth: key drivers of change

- Green Microenterprises: Providing dedicated startup and operational capital to small-scale businesses that actively drive environmental sustainability, such as localized recycling businesses, appliance repair services, and organic waste-to-fertilizer initiatives.

- Household-Level Sustainability Investments: Offering targeted consumer loans to families for purchasing resource-efficient household technologies, such as solar panels, rainwater harvesting tanks, and high-efficiency water filters.

- Community-Based Services: Financing small-scale, decentralized infrastructure projects managed by local groups, including shared community sanitation facilities, neighborhood water kiosks, and decentralized waste collection systems.

- Women and Youth as Change Agents: Positioning women and youth at the center of sustainable urban development strategies by supporting entrepreneurship, digital financial inclusion, community leadership, and environmental innovation. As some of the most active participants in microfinance initiatives, women and youth can play a critical role in promoting sustainable practices, strengthening local livelihoods, and driving long-term behavioral change within urban communities.

Together, these intervention areas illustrate how financial inclusion can simultaneously address environmental sustainability, livelihood generation, and social inclusion within urban communities.

Figure 3: Four Key Intervention Areas

| Case examples | ||

|

Case Study 10: Green Mobility Enterprises in Indonesia

|

Case Study 11: Household Water Filters in Cambodia

|

Case Study 12: Youth Urban Farming Cooperatives in Uganda

|

These intervention areas demonstrate that microfinance can support sustainable urban development at multiple scales, ranging from household investments to community-based enterprises and shared infrastructure systems.

By targeting practical environmental needs while strengthening local livelihoods, such interventions help create more inclusive, resource-efficient, and economically resilient urban communities.

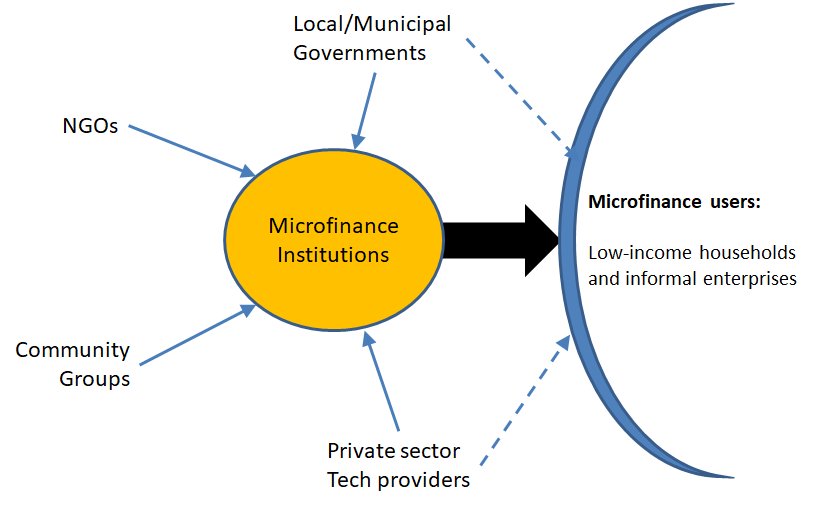

5. Role of Institutions

- Microfinance Institutions (MFIs)

- NGOs and community-based organizations

- Municipal governments

- Private sector technology providers

- Microfinance Institutions (MFIs): Responsible for designing, piloting, and scaling viable green loan products, micro-savings schemes, and localized environmental credit lines.

- NGOs and Community-Based Organizations (CBOs): Serve as the bridge to the community by delivering environmental education, technical training, and building local capacity to manage shared assets. Specifically, while NGOs can provide technical support and build capacities, CBOs can focus on local coordination and building community trust

- Municipal Governments: Coordinates the necessary policy support, offering legal recognition to informal enterprises, and linking community-level efforts to city-wide master plans. Municipal governments can also assist in other aspects such as infrastructure alignment and regulatory support

- Private Sector (Technology Providers): Developing and supplying affordable, durable, and high-quality green technologies (e.g., solar systems, water purification tools) tailored to low-income markets. The private sector, in a broader sense, can also assist in supporting innovation, creating scalable business models, lower costs through market expansion.

Figure 4: Stakeholder Ecosystem

| Case examples | ||

|

Case Study 13: Municipal Partnerships for Community Upgrading in Thailand

|

Case Study 14: NGO Support for Green Finance in Nepal

|

Case Study 15: Solar Technology Partnerships in Rwanda

|

There are a number of other entities that can also be added to this stakeholder ecosystem, including for example monitoring partners (for impact assessment and data collection), innovation hubs (for technology development and pilot testing), and training providers (for capacity building and technical skills development).

Sustainable urban development through microfinance depends on strong partnerships among financial institutions, community organizations, governments, and private sector actors.

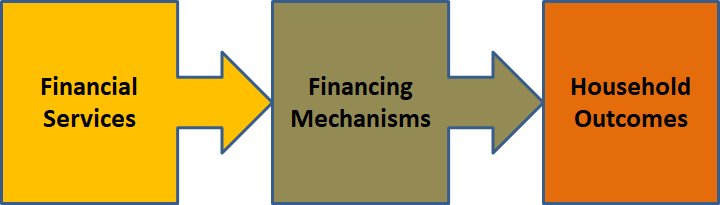

6. Tools and Mechanisms

- Green loan products

- Pay-as-you-go financing

- Group lending models

- Blended finance and subsidies

- Green Loan Products: Specialized loans are offered at concessional interest rates or with flexible repayment structures, specifically earmarked for purchasing eco-friendly technologies.

- Pay-As-You-Go (PAYG) Models: Digital mobile technology are integrated to allow households to make small, incremental payments. This could be used for clean energy or clean water utilities, eventually enabling the households to own the physical asset.

- Group Lending for Environmental Services: Joint-liability lending systems are utilized to allow community groups to collectively finance shared neighborhood resources, such as decentralized composting units or water pumps. Broadly, such systems can also be used for shared environmental infrastructure or in community resource management

- Blended Finance and Subsidies: Combining philanthropic grants or public subsidies with private microfinance capital to lower interest rates, absorb risks, and make green technologies affordable for the poorest households. These are particularly helpful in risk reduction, scalability, attracting private capital

Figure 5: Microfinance Tools and Mechanisms

| Case examples | ||

|

Case Study 16 : PAYG Solar Systems in Tanzania

|

Case Study 17: Community Water Financing in Senegal

|

Case Study 18: Green Housing Finance in Mexico

|

A number of other tools and mechanisms are also emerging in the fields of mobile banking, digital credit scoring, fintech platforms and blockchain-enabled verification that are worth exploring in future-proofing MFIs and financial inclusion programmes.

The effectiveness of microfinance in promoting sustainable urban development depends not only on access to capital, but also on the design of flexible and inclusive financial mechanisms.

By combining innovative lending approaches, digital payment systems, community-based financing structures, and targeted subsidies, financial inclusion programmes can expand access to sustainable technologies and strengthen long-term urban resilience.

7. Monitoring and Impact

- Environmental: waste reduction, energy savings

- Social: income stability, gender inclusion

- Financial: repayment rates, asset creation

- Governance: participation, representation and partnerships

| Category | Indicators |

| Environmental Indicators |

|

| Social Indicators |

|

| Financial Indicators |

|

| Governance indicators |

|

Monitoring systems should also combine baseline assessments with periodic follow-up evaluations to measure long-term environmental, social, and financial impacts.

Figure 6: Financial Inclusion Indicators

| Case examples | ||

|

Case Study 19: Community Waste Monitoring in Argentina

|

Case Study 20: Monitoring Women's Financial Participation in India

|

Case Study 21: Household Energy Monitoring in Morocco

|

Effective monitoring and evaluation systems are essential for demonstrating the broader value of microfinance within sustainable urban development. By tracking environmental, social, and financial outcomes together, institutions and communities can better understand programme impacts, improve accountability, and strengthen the long-term effectiveness of financial inclusion initiatives.

8. Looking Ahead: Policy Implication

- Climate adaptation financing

- Digital microfinance platforms

- Circular economy integration

-

Climate Adaptation Financing: Future microfinance programmes will increasingly need to move beyond short-term recovery lending toward proactive climate adaptation financing. This includes supporting households and micro-enterprises in strengthening housing structures, improving drainage systems, adopting water-saving technologies, and investing in climate-resilient livelihood activities before environmental shocks occur. Such approaches can reduce long-term vulnerability while helping urban communities prepare for increasingly frequent climate-related risks. -

Digital Microfinance Platforms: Rapid advances in digital finance technologies are transforming the delivery of financial inclusion services. Mobile banking platforms, digital payment systems, online credit assessments, and fintech-based lending models can reduce operational costs, improve accessibility, and expand outreach to underserved urban populations. These technologies also create opportunities for faster loan disbursement, improved monitoring systems, and more flexible financial products tailored to local sustainability needs. -

Circular Economy Integration: The integration of microfinance with circular economy systems offers significant opportunities for sustainable urban development. Financial inclusion programmes can support recycling enterprises, repair services, composting initiatives, and waste-to-resource businesses that reduce environmental pressures while generating local employment. Strengthening linkages between community-level enterprises and larger urban supply chains can further enhance resource efficiency and create more resilient local economies.

Looking ahead, the integration of microfinance and sustainable urban development will require greater innovation, stronger institutional collaboration, and more adaptive policy frameworks. By combining financial inclusion with climate resilience, digital technologies, and circular economy approaches, cities can create development pathways that are not only economically inclusive, but also environmentally sustainable and socially resilient.

|

|

|

Return to the Virtual Library on Microcredit Contact: Hari Srinivas - [email protected] |